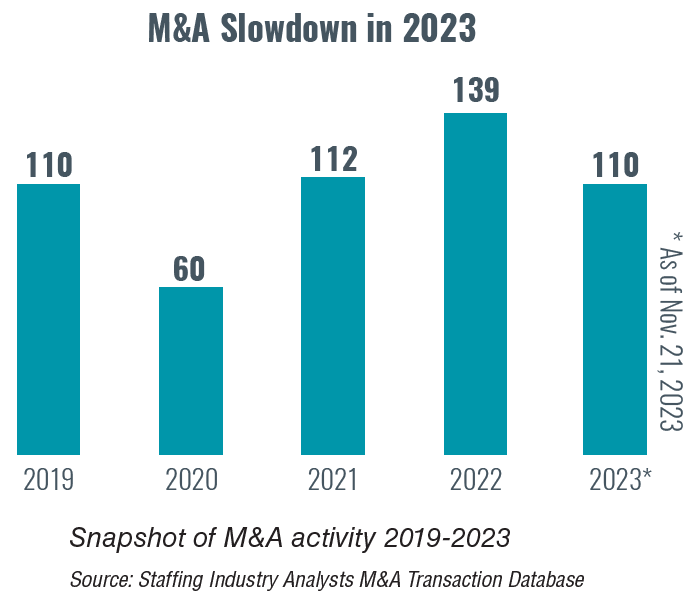

After a few years of robust deal-making activity, mergers and acquisitions in the staffing industry slowed last year as rising interest rates, cyclical headwinds and recessionary fears spurred valuation jitters. Now buyers and sellers alike are tentative. Concerns linger that the slowdown could continue.

“We saw a gap between buyer and seller expectations in 2023 for valuations as well as business performance,” says Cassidy Leventhal, principal at investment firm Achieve Partners. “Many deals failed to close as mid- and end-of-year numbers came in.” Yet there are also some positive signs. Activity in late 2023 and early 2024 was on par with pre-Covid levels. Private and private equity buyers are showing interest, especially in highly specialized and premium assets.

“Deals slowed to a trickle last year, but underlying demand didn’t — and the dam may burst in 2024,” Leventhal continues. “Companies and PE firms have been waiting over a year for the perfect time to go to market and might just decide that their next best option is now.”

Regardless, dealmakers will need to navigate a complex and evolving landscape to complete transactions successfully. Hesitation by either buyers or sellers quickly stifles M&A demand, removing a powerful tool staffing firms can use to increase market share and expand their service offerings.

Regardless, dealmakers will need to navigate a complex and evolving landscape to complete transactions successfully. Hesitation by either buyers or sellers quickly stifles M&A demand, removing a powerful tool staffing firms can use to increase market share and expand their service offerings.

“Even if interest rates fall in 2024, an increase in the demand environment will ultimately be the catalyst that propels M&A activity in the staffing industry,” says Andy Brown, managing director of Philadelphia-based investment banking firm Fairmount Partners.

Understanding emerging trends that are most likely to influence the staffing industry’s M&A landscape can be the best approach during uncertain periods. When they’re prepared, buyers can better identify potential risks and opportunities, and sellers can more adroitly adapt their strategies to maximize value and attract the right buyers.

As SIA Chief Analyst Barry Asin notes, “There are always bright spots, even in a down market.”

Here’s what both sides need to know.

A Focus on Smaller Strategic Deals

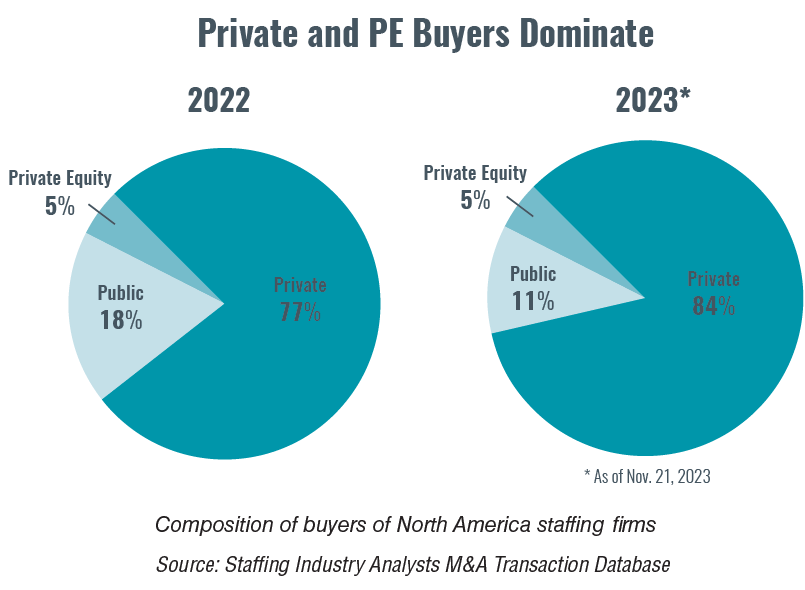

With large public companies mostly sitting on the sidelines, private buyers have been dominating. In many cases, they have focused their attention on firms that generate under $50 million in revenue, where financing is easier to attract.

“Private buyers are looking to acquire add-on services and firms with sticky revenue in terms of repeat customers and contingent workers with unique professional skills that are hard to replicate or steal,” explains Dexter Braff, president of Braff Group, a Pittsburgh-based M&A advisory firm.

In healthcare, for instance, firms that service a small, protected segment of the market — such as surgical or cardiac care centers — are highly sought after, Braff notes. The most significant recent change, however, is that buyers are seeking firms that place revenue generators, not overhead generators — such as locum tenens physicians or allied health professionals.

Recent Attractive M&A Targets

Recent Attractive M&A Targets

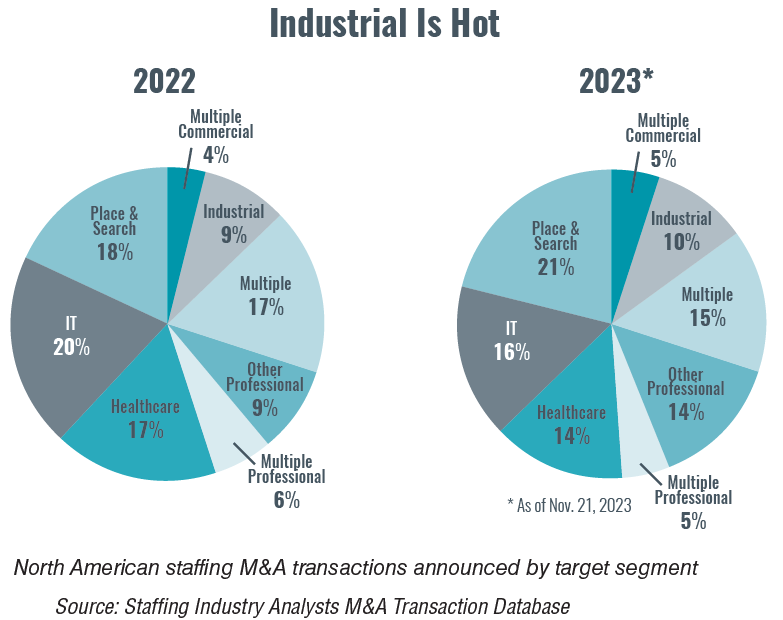

The recent headwinds have clearly impacted the M&A market, with some staffing segments and specialties faring much better than others.

“While each segment has its own dynamic, the upswing in manufacturing, shipping and distribution has created a huge demand for industrial staffing firms in the South and Midwest and kept valuations steady,” says Eric Allison, managing partner at M&A consulting firm Staffing Venture Capital.

Steady declines in direct work engagement and slight declines in IT and healthcare M&A in 2022 were offset by increasing activity in executive search, direct placement and other professional staffing segments including finance and accounting, according to SIA data.

Deep Dive Due Diligence

After a flurry of M&A activity in 2021 led to average multiples of about 11.7 times EBITDA, buyers have been worried about overpaying for staffing acquisitions. As a result, due diligence is taking 30 to 60 days longer, and purchase price multiples have been pushed into correction mode.

“We have whiplash from how quickly things change in this market,” Braff notes. “We’re getting deals to the 10-yard line but seeing buyers get cold feet and pull out.”

“We have whiplash from how quickly things change in this market,” Braff notes. “We’re getting deals to the 10-yard line but seeing buyers get cold feet and pull out.”

Today’s buyers are often supported by as many as eight third-party advisors who examine such issues as cybersecurity risks, contingent worker classification and overtime compliance, cultural impact and even management retention and succession programs. Revenue sustainability, including client concentration, relationships and contracts, has come under increasing scrutiny as well. As an example, Allison says that generating more than 25% of revenue from a small number of high-volume customers or managed service providers (MSPs) will result in a lower valuation.

Evolving Deal Pricing and Terms

While the appetite to acquire premium assets remains strong, deal details are reflecting current market realities.

Buyers are offering higher levels of earnout and expecting sellers to carry notes as opposed to going out to banks, industry experts say. At the same time, sellers of premium assets can command all cash or 90% cash at closing with a one-year earnout. In contrast, sellers of average assets can expect to receive about 50% to 80% of the purchase price in cash with one to three-year earnouts. Overall, however, “strong companies that have a solid footprint in a defensible niche will always be valuable,” SIA’s Asin says.

Tips for Succeeding in an Evolving Market

Given the headwinds, prospective buyers and sellers that embrace the following strategies stand the best chance of coming out on top in 2024, industry experts say.

For Prospective Sellers

Get your house in order. Position for 2025 by hiring outside experts to review your firm’s financials and conduct a quality of earnings assessment, compliance audits and legal assessments. Making corrections now can prevent due diligence surprises and delays.

Invest in technology. Investments in technology can turn an ordinary staffing firm into an attractive target. For instance, online talent platforms will continue to build scale by acquiring traditional staffing businesses. And speed, efficiency and computer-aided compliance will become more critical in driving valuations going forward.

Establish cultural differentiation. Buyers are looking for a differentiated culture that people want to join but which also creates high levels of performance and tenure through internal growth and promotions, says Fairmont Partners Managing Director Andy Brown.

Prevent talent loss. Ensure the continuity and success of your organization by putting non-compete and non-solicitation agreements in place and developing a comprehensive plan to retain key members of your management team.

Become proficient at forecasting. Buyers are willing to reward sellers for predicting a rosy future as long as they aren’t based on gut instinct. Use past and real-time data to predict future supply and demand, pricing and margins on a quarterly basis.

Staffing firms should “build 12-month targets they can stand by,” says Cassidy Leventhal, principal at Achieve Partners. “The average deal process lengthened in 2023, and sellers were able to see more months of performance than the pre-Covid average. If this trend holds, sellers will want to commit to targets that are exciting but achievable and allow them to deliver great news throughout a process.”

For Prospective Buyers

Assemble the right team. Engage investment bankers, attorneys and CPAs who understand the industry’s pricing, competition and margin structure. Know the current market. Determine the fair value of the target company based on its assets, liabilities, financial performance, market position, execution of staffing fundamentals and intangible assets that matter most like culture, leadership and relationships with clients and contingent staff.

Look for alignment on multiple levels. Determine the ideal buyer profile for a prospective asset and whether your company is the right fit. The best M&A deals provide win-win solutions and value for both the buyer and seller.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}